Vedanta Records Best-Ever Performance, Waaree Energies Falls 10% Despite 101% Increase In Net Profit

- Share.Market

- 5 min read

- Published at : 30 Apr 2026 01:57 PM

- Modified at : 30 Apr 2026 01:59 PM

Share

Article Link Copied : https://www.share.market/buzz/news/vedanta-best-ever-performance-waaree-energies-falls/

53 Companies, including Adani Power, Vedanta, Indian Bank, Waree Energies, and Federal Bank, reported their results yesterday.

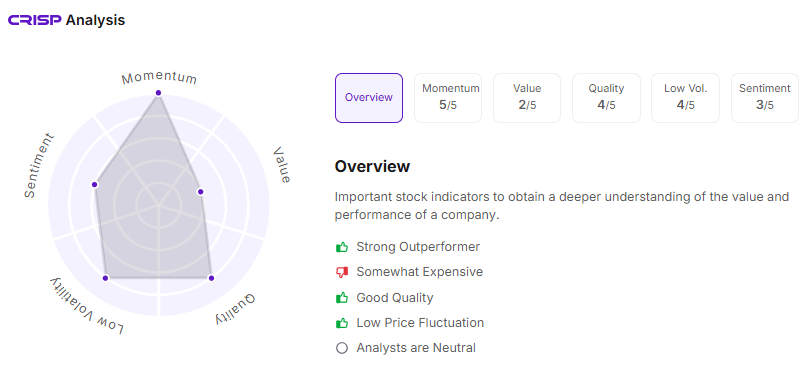

Adani Power Ltd.

| Metric | FY 2025-26 (Audited) in ₹ | FY 2024-25 (Previous) in ₹ | % Change (YoY) |

| Revenue from Operations | 54,240.52 Cr | 56,203.09 Cr | -3.49% |

| Net Profit (PAT) | 12,971.08 Cr | 12,749.61 Cr | +1.74% |

| Earnings Per Share (EPS) | 6.62 | 6.46 | +2.48% |

- The company’s management highlighted a robust capacity expansion pipeline of 23.7 GW, focusing on securing long-term Power Purchase Agreements (PPAs) to ensure sustainable cash flows.

- During the financial year (on September 22, 2025), Adani Power successfully implemented a 1:5 Stock Split, where the face value of each equity share was reduced from ₹10 to ₹2.

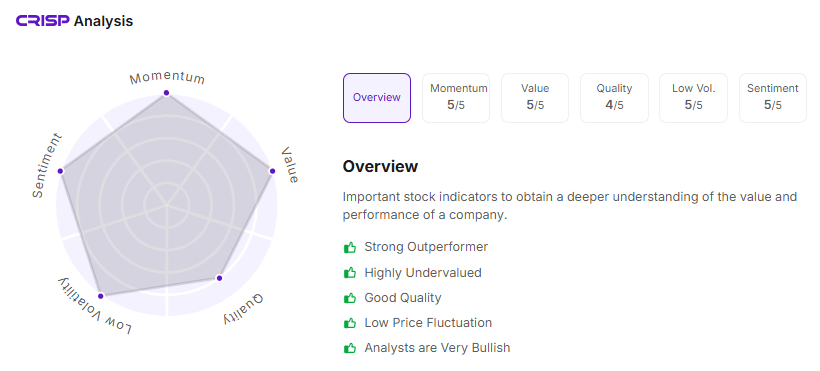

Vedanta Ltd.

| Metric | FY 2025-26 (Audited) in ₹ | FY 2024-25 (Previous) in ₹ | % Change (YoY) |

| Revenue from Operations | 78,437 Cr | 62,717 Cr | +25.06% |

| Net Profit (PAT) | 25,096 Cr | 20,535 Cr | +22.21% |

| Earnings Per Share (EPS)* | 64.18 | 52.52 | +22.20% |

- Vedanta recorded its highest-ever annual Revenue, EBITDA, and PAT, driven by record operational performance across its aluminium and zinc portfolios.

- The company significantly strengthened its balance sheet, with the Net Debt-to-EBITDA ratio improving to 0.95x, down from 1.22x in the previous year.

- It achieved record production levels, including 2.46 million tonnes of aluminium and 1.1 million tonnes of mined metal at Zinc India.

- The company is on the verge of a massive structural change, with the demerger into five separate listed entities (Aluminium, Power, Oil & Gas, Steel, and the Residual Entity) scheduled to be effective from May 1, 2026.

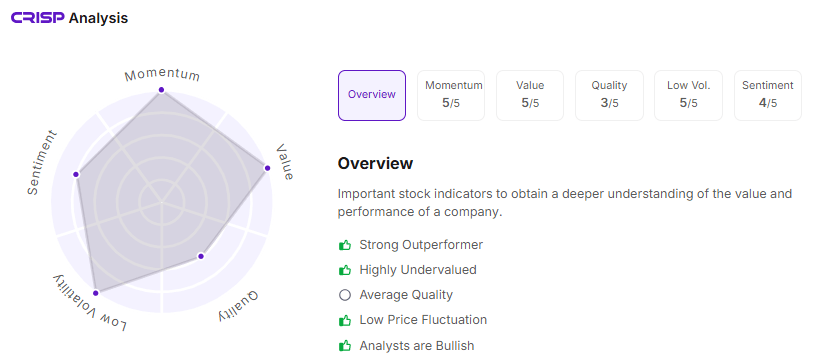

Indian Bank

| Metric | FY 2025-26 (Audited) in ₹ | FY 2024-25 (Previous) in ₹ | % Change (YoY) |

| Total Income (Revenue) | 78,332.70 Cr | 72,050.88 Cr | +8.72% |

| Net Profit (PAT) | 11,704.28 Cr | 11,261.47 Cr | +3.93% |

| Earnings Per Share (EPS) | 86.89 | 83.61 | +3.93% |

- The bank saw a sharp improvement in asset quality, with the Gross NPA ratio falling to 1.98% (from 3.09% last year) and Net NPA maintaining a very low profile at 0.15%.

- Provisions (other than tax) dropped to ₹3,514.64 Cr from ₹4,214.10 Cr in the previous year, directly boosting the bottom line as the bank cleaned up its legacy bad loans.

- The Capital Adequacy Ratio (CRAR) remained strong at 17.93%, well above regulatory requirements, providing a solid cushion for future lending expansion.

- The Board of Directors has recommended a final dividend of ₹18.25 per equity share (182.50% of the face value of ₹10) for the financial year 2025-26.

- The Board also approved a plan to raise equity capital up to ₹5,000 crore (including premium) through various modes like QIP, Rights Issue, or FPO to fund future growth.

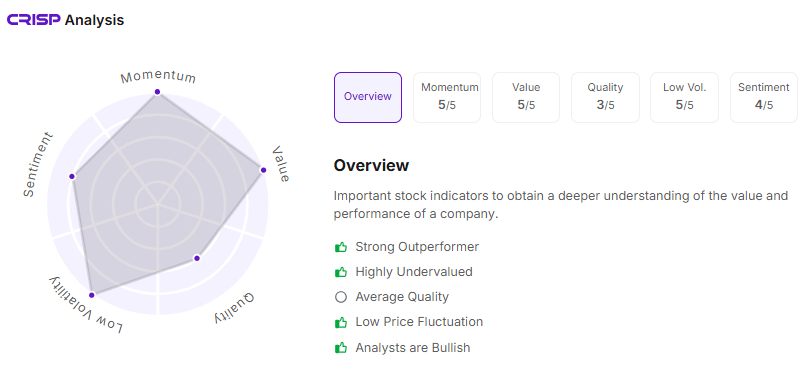

Federal Bank Ltd.

| Metric | FY 2025-26 (Audited) in ₹ | FY 2024-25 (Previous)in ₹ | % Change (YoY) |

| Total Income (Revenue) | 34,272.42 Cr | 32,030.25 Cr | +7.00% |

| Operating Profit (EBITDA Eqv.)* | 7,834.22 Cr | 6,507.03 Cr | +20.40% |

| Net Profit (Group PAT) | 4,345.30 Cr | 4,158.85 Cr | +4.48% |

| Earnings Per Share (EPS) | 17.67 | 16.98 | +4.06% |

- While operating performance was stellar, the bottom-line growth (PAT) was restricted to 4.5% because the bank chose to more than double its provisions (from ₹919 Cr to ₹1,970 Cr), likely to further strengthen the balance sheet against potential slippages.

- The consolidated profit was boosted by strong performances from subsidiaries, including Fedbank Financial Services (Fedfina) and the bank’s life insurance associate, Ageas Federal.

- The bank completed the issuance of over 27 crore warrants to Ageas Topco and increased its stake in Ageas Federal Life Insurance, consolidating its position in the insurance space.

- A final dividend of ₹1.20 per equity share (60% of the face value of ₹2) for FY 2025-26, subject to shareholder approval.

Waaree Energies Ltd.

| Metric | FY 2025-26 (Audited)in ₹ | FY 2024-25 (Previous)in ₹ | % Change (YoY) |

| Revenue from Operations | 26,536.77 Cr | 14,444.50 Cr | +83.72% |

| EBITDA (Equivalent)* | 6,616.79 Cr | 3,123.20 Cr | +111.86% |

| Net Profit (PAT) | 3,884.15 Cr | 1,928.13 Cr | +101.45% |

| Earnings Per Share (EPS) | 129.10 | 68.24 | +89.18% |

The 10% decline in Waaree Energies share price following the Q4 FY26 results is primarily attributed to margin compression. While the company delivered record growth, it appears to have fallen short of specific investor expectations regarding operational profitability.

Sequential Drop: Operating EBITDA margins fell from 25.49% in Q3 FY26 to 18.59% in Q4 FY26. This 690-basis-point drop sequentially signalled a significant deceleration in profitability despite higher sales.

Increased Operational Costs impacted the bottomline:

- Cost of Materials: Surged from ₹2,409.57 Cr in Q4 FY25 to ₹6,738.63 Cr in Q4 FY26.

- Other Expenses: “Sales, administration and other expenses” nearly doubled YoY to ₹506.93 Cr, further eating into margins.

Share

Article Link Copied : https://www.share.market/buzz/news/vedanta-best-ever-performance-waaree-energies-falls/