Dr. Reddy’s Reports Q2 FY26 Growth: Strong Branded Markets Offset North America Headwinds

- Share.Market

- 3 min read

- Published at : 24 Oct 2025 06:59 PM

- Modified at : 30 Oct 2025 07:06 PM

Dr. Reddy’s Laboratories Ltd. announced its financial results for the second quarter ended September 30, 2025 (Q2 FY26), reporting near double-digit revenue growth and strong profit, primarily driven by its branded markets and strategic acquisitions.

Revenues for Q2 FY26 stood at ₹8,805 crore, reflecting a 9.8% growth year-on-year (YoY) and 3% growth sequentially. This was driven by broad-based performance, moderated by softness in the US generics market.

EBITDA was ₹2,351 crore, representing 26.7% of revenues. EBITDA grew 3% both YoY and sequentially. The company’s underlying EBITDA margin, after adjusting for one-off provisions, was 27.5%.

Profit After Tax (PAT) attributable to equity shareholders was ₹1,437 crore, or 16.3% of revenues. PAT grew 14% YoY, although it saw only a 1% sequential increase.

Global Generics revenues accounted for 89% of the total, growing 10% YoY.

India delivered double-digit growth, with revenues of ₹1,578 crore (up 13% YoY and 7% sequentially), driven by new brand launches, improved pricing, and higher volumes. Notably, the company launched two novel Gastro-Intestinal drugs: Tegoprazan as ‘PCAB®’ and Linaclotide as ‘Colozo®’.

Europe saw significant growth, with revenues of ₹1,376 crore (up 138% YoY and 8% sequentially). This surge was underpinned by the recently acquired Nicotine Replacement Therapy (NRT) business, with integration progressing well.

Emerging Markets revenues were ₹1,655 crore, up 14% YoY and 18% sequentially, fueled by new product launches and favorable foreign exchange movements.

North America revenues were ₹3,241 crore, declining 13% YoY and 5% sequentially. This decline was due to price erosion for specific products and lower sales of Lenalidomide.

PSAI (Pharmaceutical Services and Active Ingredients) revenues were ₹945 crore, growing 12% YoY and 16% sequentially, driven by new product launches and favorable forex.

The company made a key strategic move by acquiring Stugeron® and related brands for 18 markets in APAC (including India & Vietnam) and EMEA, augmenting its branded markets portfolio.

The IND application for COYA 302 was accepted by the USFDA, and the company received a positive opinion from the EMA’s CHMP for its denosumab biosimilar candidate. Approval for Semaglutide injection in India was also recommended by the SEC under CDSCO.

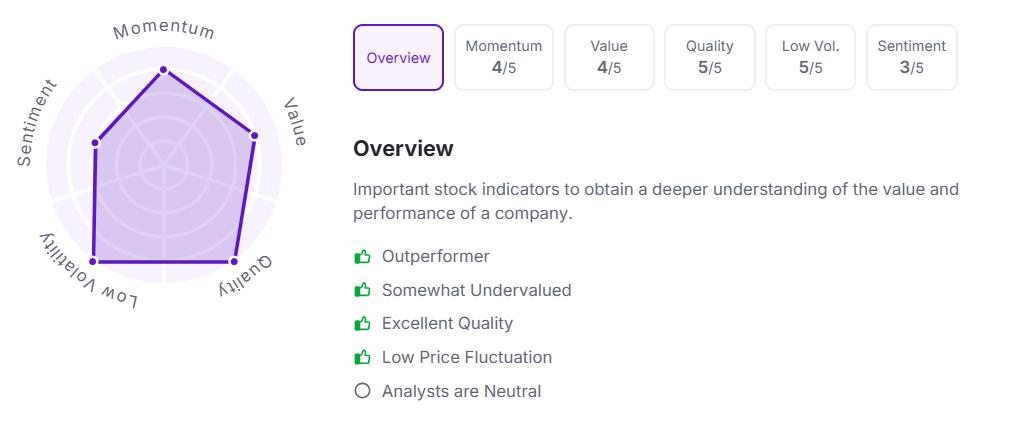

Let’s take a look at its Factor Analysis scores:

Note: The stock price mentioned is as of 3:30 pm.