Did Eternal’s Revenue Really Jump By 186%?

- Share.Market

- 2 min read

- Published at : 04 May 2026 01:50 PM

- Modified at : 04 May 2026 03:04 PM

Zomato’s parent company Eternal’s consolidated adjusted revenue jumped 186% in Q4FY26.

At first glance, the numbers look very strong.

The company reported a consolidated adjusted revenue of ₹17,680 crore in Q4, and EBITDA also rose by 160% to reach ₹429 crore.

However, it is important to understand one key point: this growth isn’t just from higher demand; it is also due to a change in Quick Commerce accounting.

The company now uses a 1P model, where the full value of the goods sold is included in the revenue, rather than just the commission earned.

If we look at “like-for-like” (LFL) growth—meaning a comparison on the same basis—the actual growth is around 64%, which is still quite strong.

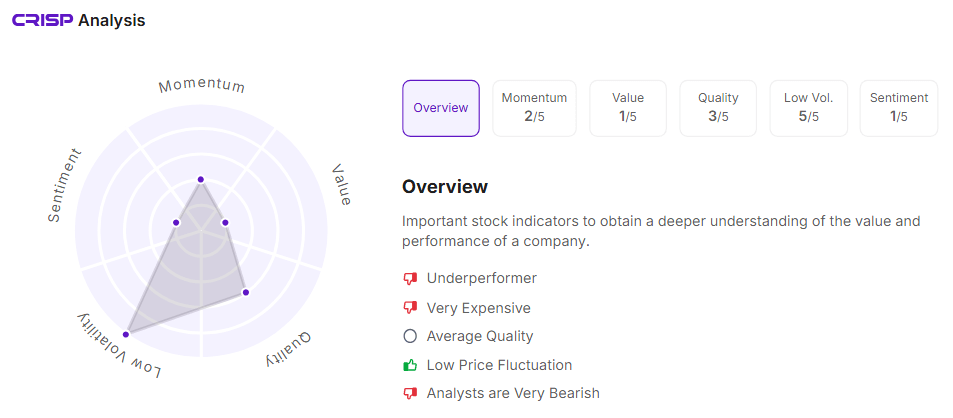

Eternal’s CRISP Analysis

Another important metric is Net Order Value (NOV), which is simply how much customers spent after discounts. Interestingly, the overall B2C NOV grew by 54%, proving that real demand is growing at a healthy pace.

Segment Breakdown

- Blinkit: Remains the biggest growth driver with 95% YoY growth. They added 216 new stores, and EBITDA improved to ₹37 crore, which is a positive sign for profitability.

- Food Delivery: Shows stable growth at 18.8% YoY, with margins improving to 5.5%.

- New Strategy: The company introduced a ₹99 free delivery threshold to attract budget-conscious customers.

Overall, the company’s multiple businesses are scaling and improving simultaneously. However, competition is becoming aggressive, especially in the Quick Commerce space.

The big question now is: will this growth momentum continue, or will the competition slow it down?