Bharti Airtel Shares Shed 4% After Announcing A ₹20,000 Crore NBFC Expansion — Here’s Why

- Share.Market

- 2 min read

- Published at : 24 Feb 2026 12:40 PM

- Modified at : 26 Feb 2026 03:33 PM

Shares of telecom giant Bharti Airtel shed 4% on Tuesday’s trading session, emerging as one of the top laggards on the Nifty 50. The stock touched an intraday low of ₹1,921.80 on the NSE, marking its steepest single-day decline in over three months.

A Landmark ₹20,000 Crore NBFC Foray By Airtel Money

According to an exchange filing, Bharti Airtel is set to significantly scale its financial services footprint through its subsidiary, Airtel Money. It has announced a massive capital infusion of ₹20,000 crore to be injected over the next few years.

Key Details

- Capital Structure: Bharti Airtel will contribute 70% of the capital, with the remaining 30% being infused by the promoter group through Bharti Enterprises.

- Regulatory Milestone: The company confirmed it received the formal NBFC (Non-Banking Financial Company) license from the Reserve Bank of India (RBI) on February 13, 2026.

- Operational Scale: Airtel’s digital lending platform has already achieved a “hyperscale” status, having disbursed over ₹9,000 crore via its existing Lending Service Provider (LSP) model.

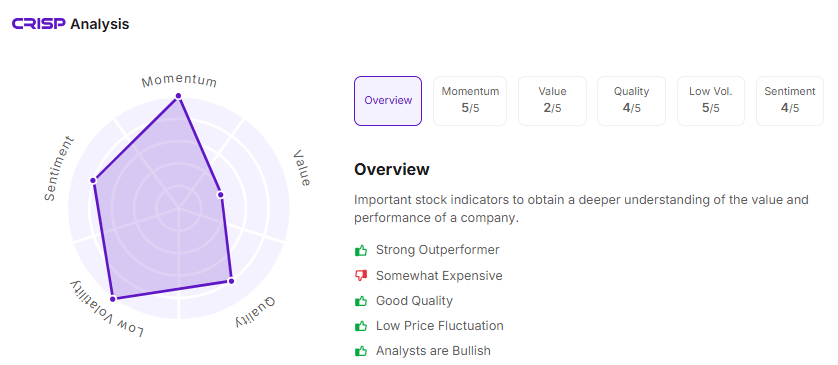

Let’s take a look at its CRISP Analysis:

Strategic Shift vs. Capex Concerns

The long-term rationale is to tap into India’s vast credit gap—where the formal credit-to-GDP ratio stands at just 53%.

Gopal Vittal, Executive Vice Chairman of Bharti Airtel, stated in the release that the expansion aims to build a “differentiated, future-ready digital lending business.” The company plans to leverage its massive pool of over 500 data scientists and its existing customer ecosystem to offer secure credit.

However, as per media reports, analysts noted that while the group has been “prudent in digital allocation” in the past, an NBFC is a fundamentally different, capital-heavy beast compared to a pure-play digital distribution platform. The shift from a “distributor” (LSP) to a “lender” (NBFC) implies that Airtel will now carry credit risk on its own books, necessitating higher capital buffers and potentially weighing on the consolidated return ratios in the initial phase.