Why The Silver Price Is Soaring: The Hidden Boom Investors Can’t Ignore

- Share.Market

- 13 min read

- 18 Oct 2025

Something big is happening in the precious metals world. You’ve probably noticed gold making headlines, but the real story is silver.

Gold, the world’s ultimate haven, is trading at record highs above $4,100 per ounce.

But silver has quietly staged an even bigger breakout, crossing $51 per ounce globally, with Indian silver prices touching historic highs.

However, beneath this glittering rally lies a hidden trap that every Indian investor needs to understand before buying in.

In this piece, we’ll break it down simply and clearly:

- Why are silver prices soaring right now?

- Can this rally continue?

- How should you invest smartly

Silver: Gold’s High-Growth Sibling with an Industrial Engine

Silver is a powerful asset because it has two motors running at the same time.

It gets all the same benefits from global worries and lower interest rates as gold, but its price is supercharged by a second, unique engine: its essential role as an industrial metal.

This dual identity makes silver not just a store of value, but a critical part of the 21st-century technology and clean energy revolution.

More Than Money: Silver’s Dual Identity

Unlike gold, where almost all the metal ever mined is kept as jewelry or investment, a large portion of silver is used up by factories every year.

Over half of all annual silver demand comes from industrial applications.

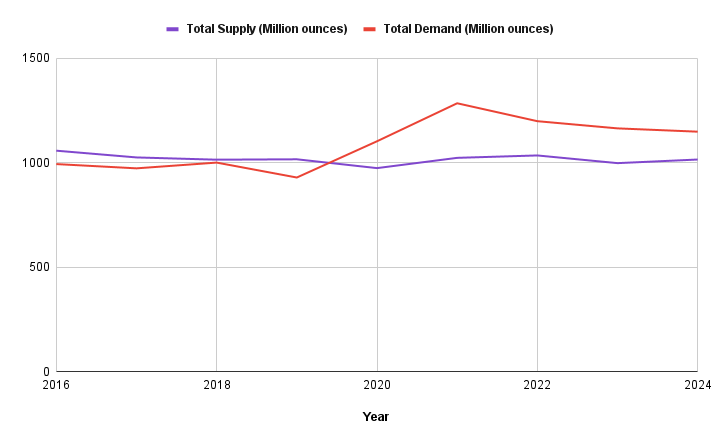

Silver Supply and Demand

This is the fundamental difference: while gold shines when the economy is weak (due to fear), silver has extra support from real, tangible demand from manufacturers, which anchors its value to technological growth.

This is why silver tends to be more volatile than gold, but also has the potential for much higher returns.

The Green Revolution’s Silver Vein

Silver’s industrial demand is focused on the world’s fastest-growing, most critical sectors. It is often irreplaceable in these applications because of its unique properties, especially its unmatched ability to conduct electricity.

Longer-Term Industrial Demand Indicators

Solar Panels (Photovoltaics)

The shift to renewable energy is the biggest single driver of silver demand. Silver paste is an absolutely necessary component in solar cells to conduct the electricity captured from the sun.

- The solar sector alone now consumes nearly 20% of the entire global silver supply.

- As nations race to meet their climate goals, this demand is projected to grow exponentially. Some long-term forecasts even suggest that solar manufacturing could eventually consume almost all of the world’s current silver reserves, highlighting an unsustainable and therefore bullish demand trend.

Electric Vehicles (EVs)

The transition to electric cars is another massive consumer of silver.

- Silver is essential in EV batteries, critical high-conductivity electrical connections, and advanced safety systems.

- The demand for silver from the EV sector will climb consistently with global electric vehicle adoption rates.

Advanced Electronics and Connectivity

Beyond clean energy, silver is the cornerstone of modern tech. It’s found in everything from smartphones and semiconductors to the complex hardware required for 5G networks and Artificial Intelligence (AI). Every new technological leap creates a new, resilient stream of demand for the metal.

The Structural Supply Crisis

Now here’s where it gets serious: silver demand is outpacing supply and not just for a few months.

Silver Supply & Demand Mismatch

- Demand > Supply: For four years in a row (2021-2024), the global demand for silver has been significantly higher than the combined supply from new mines and recycling.

- Inventory Drain: This chronic shortfall is systematically draining the world’s existing above-ground inventories of silver bullion, especially in major storage centers like London.

- Explosive Potential: This tightening physical market is the key ingredient missing in previous rallies. It creates the perfect condition for prices to become extremely volatile and shoot sharply upward as major industrial buyers and large investors compete for a shrinking pool of available metal.

This fundamental shortage is what truly sets silver’s bull case apart from gold’s, suggesting a potentially much more explosive long-term price path.

What This Means for Your Portfolio

The massive rally in gold and silver doesn’t happen in a silo; it has immediate effects across everything you own, including your stocks, bank deposits, and direct metal holdings.

Understanding how precious metals interact with your other assets is crucial, especially given the sudden and unique problem that has emerged in the Indian silver market.

The metals act in two key ways: they protect your wealth when the market falls, and they change the attractiveness of other assets.

Stocks (Sensex/Nifty)

The relationship with the Indian stock market is usually a great balance for investors:

- The Protective Hedge (Negative Correlation): This is the most celebrated role. Over the past year, while the main Indian indices (Nifty 50 and Sensex) delivered nearly flat returns, both gold and silver gave returns exceeding 50%. When the stock market gets volatile or falls (due to fear or instability), money naturally flows out of risky assets like stocks and into safe havens like gold. This protective dynamic helps cushion your entire portfolio against a stock market downturn.

- The Sectoral Boost: While the overall market may be flat, a strong rally in metal prices can directly help related businesses. For example, companies that mine or refine metals may see their profits jump. However, the effect on jewelry companies is mixed: they profit from the gold they already own, but record-high prices can scare away customers looking to buy new ornaments, which can slow down their sales growth.

Debt and Fixed Income

In the current environment, precious metals have become much more appealing compared to traditional, interest-paying investments like government bonds and fixed deposits.

- Low-Yield World: The US Federal Reserve is signaling that it plans to cut interest rates soon. Lower interest rates mean the returns you get from bonds and debt (the real interest rate) are low or falling.

- The Opportunity Cost Shrinks: Since gold and silver don’t pay interest, they compete directly with these debt instruments. When the interest paid by bonds falls, the money you “give up” to hold gold shrinks. This makes non-interest-paying assets like gold and silver comparatively much more attractive, pulling capital away from debt markets. A clear example in India is the high demand for Sovereign Gold Bonds (SGBs), where investors are eagerly paying extra just to secure the government-backed gold exposure.

The Hidden Trap: India’s Silver “Premium Problem”

Here’s the part most investors miss.

While silver looks strong globally, Indian buyers are currently paying a steep premium between 10% and 18% above global prices.

That’s not normal.

Historically, the premium was small and stable. But in 2025, it spiked sharply, even touching 12% intraday in some cases.

Decoding the Price Gap

This is not a normal market condition. Historically, the price difference (premium) in India over the import cost (global price + duties) is very small.

Recently, however, this premium has exploded, with reported intraday spikes as high as 12%. This shows a complete breakdown in the normal trade mechanisms that usually keep local and global prices in line.

Why the Price is Squeezed

This unprecedented premium is the result of a “perfect storm” hitting the Indian market:

- Explosive Local Demand: The peak festive season of Dhanteras and Diwali has led to a frantic surge in physical buying from jewelers, dealers, and retail consumers scrambling for stock.

- Global Supply Shortage: This local rush is happening when the global market is already experiencing a structural deficit and key world inventories are at multi-year lows.

- Import Bottlenecks: India relies heavily on imports. Because of global tightness, our silver imports plunged by over 40% in early 2025. This has created an acute, temporary physical shortage within the country.

Is Silver Still Worth Investing In?

To understand this, let’s look at the two things:

A Look Back: The 1980’s and 2011 Rally

To see silver’s explosive power, we can look back at the rally.

The historical price trajectory of silver, as evidenced by its dramatic spikes in 1980 and 2011, paints a picture of extreme volatility, earning it the nickname “poor man’s gold.”

However, comparing the forces that drove those earlier bubbles to the structural changes driving the current 2020s rally reveals a profound shift in market fundamentals.

Silver Price Trend (1975 – 2025)

The 1980 Peak and the Folly of Cornering

The 1980 silver spike was a classic speculative bubble rooted in market manipulation. The Hunt brothers attempted to corner the silver market, accumulating an estimated one-third of the world’s private physical silver supply and heavily leveraged futures contracts.

- Reason for the Fall: The fall was a direct, targeted regulatory action. The COMEX changed the rules (Silver Rule 7) to limit leverage and forced massive margin calls on the Hunts. When they couldn’t meet the calls, their forced liquidation created an immediate, cataclysmic supply flood (“Silver Thursday”), demonstrating that the price had no organic demand floor.

The 2011 Peak and the Monetary Rotation

The 2011 run was a monetary event. Following the 2008 Financial Crisis, investors flocked to precious metals as a hedge against unprecedented money printing (QE) and sovereign debt fears. Silver, being the “high-beta” version of gold, magnified those gains.

- Reason for the Fall: The price fell sharply because the core driver was emotional and financial leverage, not physical consumption. When the immediate crisis threats subsided in late 2011, and market stability returned, the capital that had flowed into precious metals began to rotate back into equities and debt instruments, starving silver of its investment demand and sending the price tumbling.

The 2020s: A Structural, Industrially-Driven Rally

The current silver rally stands apart because the dominant driver is physical industrial demand tied to the global energy transition a structural shift that is non-negotiable and multi-decade in scope.

First, Silver is the most electrically conductive metal and is mission-critical for the “Green Economy”:

On the otherside, this industrial surge has created a persistent, multi-year supply deficit. Since 2021, global silver demand has consistently exceeded supply (mine production plus recycling). This structural shortage means that above-ground inventories (vault stocks) are being systematically depleted.

- Unlike 1980: This demand is from factories and production lines, not futures traders.

- Unlike 2011: The metal is being consumed and largely unrecoverable (e.g., in solar panels until end-of-life), establishing a powerful floor price for the metal.

In addition to the industrial story, the supportive monetary factors from 2011, namely high government debt, persistent inflation concerns, and a pivot towards anticipated rate cuts are still in play, providing a powerful dual tailwind.

The Gold-Silver Ratio (GSR)

One of the simplest yet most powerful tools for deciding if silver is cheap or expensive compared to gold is the Gold-Silver Ratio (GSR).

The GSR simply measures how many ounces of silver it takes to buy one ounce of gold.

- Ancient History: For thousands of years, governments often fixed this ratio around 12:1 to 16:1.

- Modern Average: Since governments stopped fixing the price, the ratio has usually swung between 50:1 and 70:1.

Gold Silver Ratio

The current Gold-Silver Ratio is high, standing above 80:1. Historically, a high ratio is a clear signal that silver is undervalued relative to gold.

For long-term investors, periods when the GSR is high have often been the best times to buy silver.

The expectation is that the ratio will eventually “mean-revert,” or return closer to its historical average. This reversion is usually achieved because:

So, the silver market is currently in a state of fundamental revaluation.

The forces driving the price today are distinct from the speculative euphoria of 1980 and the purely monetary reaction of 2011.

The confluence of a deep, structural supply deficit created by non-recyclable industrial consumption and a historically high Gold-Silver Ratio suggests the price is being driven by concrete scarcity rather than transient sentiment.

This framework positions silver at the intersection of critical industrial utility and macro-economic hedging, making its current trajectory an evolution toward a more fundamentally supported price level.

What Investors Should Keep in Mind

The current silver environment offers both opportunities and challenges, but it requires context and caution rather than quick decisions. Understanding the market structure, timing, and underlying drivers is essential before forming any investment view.

The Premium Distortion in India

At present, domestic silver prices in India are trading significantly above international benchmarks. This difference, often called the import or retail premium, has widened to unusually high levels, reflecting a temporary imbalance between physical demand and available supply.

Such distortions usually emerge when festival-driven demand coincides with import delays or global supply tightness. For investors, this highlights how local price behavior can deviate sharply from global trends, affecting short-term affordability and liquidity.

Market Access and Exposure Channels

Silver exposure can take multiple forms from physical bullion and jewelry to exchange-traded products, commodity futures, or shares of silver-related companies. Each of these carries different cost structures, liquidity profiles, and risk sensitivities to global price movements.

Understanding these channels helps investors recognize that not all “silver investments” move in the same way or at the same pace, especially during volatile periods.

The Importance of Time Horizons

Silver’s price pattern historically alternates between long periods of consolidation and sudden, sharp upswings. These movements are often linked to shifts in monetary policy, industrial demand, and market sentiment.

Rather than viewing short-term rallies in isolation, it is useful to analyze silver within multi-year cycles, comparing it with historical episodes like 2010–2011 or earlier bull phases.

Relationship with Gold and Broader Portfolios

Gold and silver often share similar macroeconomic drivers such as interest rate trends, inflation expectations, and investor risk appetite, but they behave differently.

Gold tends to respond more to financial market uncertainty, while silver also reflects changes in industrial output and technology adoption.

This dual nature means that silver’s movements can be more volatile yet sometimes more responsive during global growth phases.

In a diversified portfolio, such characteristics influence how silver interacts with equities, debt, and other assets, shaping the overall balance between stability and growth potential.

Monitoring Structural Indicators

Several long-term metrics provide insight into silver’s position within the broader commodities cycle:

- The Gold–Silver Ratio (GSR): Indicates relative valuation between the two metals.

- Mine Production and Recycling Data: Offer clues about supply constraints or recovery potential.

- Industrial Consumption Trends: Especially in solar energy, electronics, and electric mobility, which shape sustained demand.

- Monetary Policy and Real Interest Rate: Often guide the direction of precious metal prices globally.

Together, these indicators can help investors form a reasoned understanding of silver’s evolving role not as a quick trade, but as a reflection of deeper economic and industrial transitions.

Final Thoughts

Silver’s recent performance reflects more than just a price rally; it signals a deeper shift in global economic and industrial patterns.

The metal’s dual role, as both a traditional store of value and a critical industrial input, places it at the intersection of monetary policy, technological innovation, and sustainability-driven growth.

While gold continues to act as a conventional hedge against uncertainty, silver’s increasing use in renewable energy systems, electric mobility, and advanced electronics underscores its expanding relevance in the real economy.

At the same time, the widening gap between global and domestic prices in India highlights how local market dynamics, import dependencies, and festive consumption cycles can temporarily distort broader trends.

Ultimately, the silver market today represents a convergence of financial sentiment and industrial transformation.

Its trajectory in the coming years will likely be shaped by how these two forces, economic caution and technological progress, continue to interact on the global stage.