Liquidity Trap: Definition, Causes & Economic Impact Explained

- Share.Market

- 4 min read

- 23 Apr 2026

Highlights

- Understand what defines a liquidity trap and why they occur

- Learn how to overcome a liquidity trap

- Discover real-life examples of a liquidity trap

Introduction

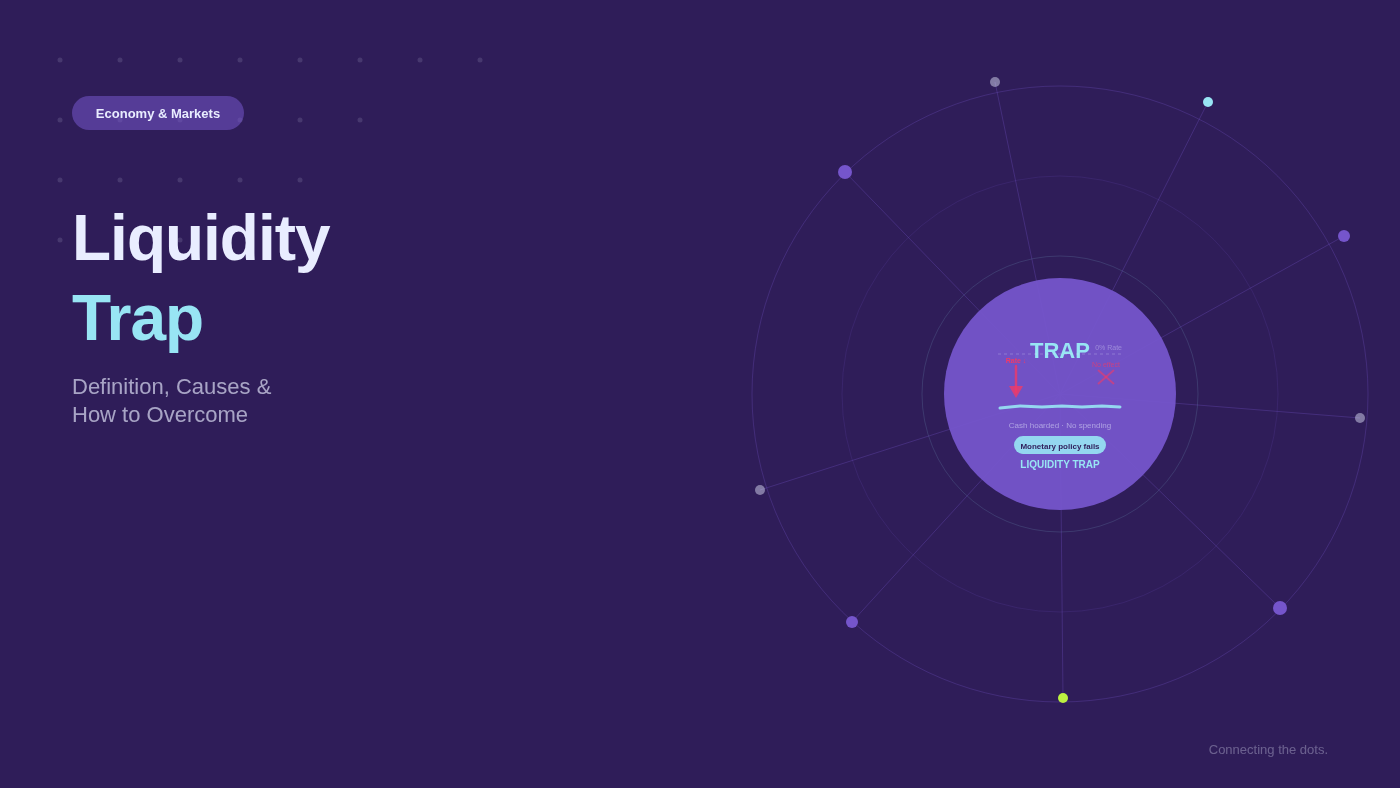

A liquidity trap occurs when interest rates are already very low, yet people still choose to save rather than spend or invest. Even if central banks pump more money into the economy, individuals prefer holding cash for safety. As a result, interest rate cuts lose their power to stimulate growth, and economic activity slows despite higher liquidity in the system.

What Defines a Liquidity Trap

A liquidity trap represents a situation where monetary policy loses its stimulative power. When interest rates fall to zero or near-zero, central banks cannot cut them further. Yet people choose cash over investments, fearing deflation or economic uncertainty.

The term originated from Keynesian economics, describing conditions where increased money supply fails to lower interest rates or stimulate demand. Cash becomes the preferred asset despite yielding no return.

Why Liquidity Traps Occur

A liquidity trap occurs when people prefer holding cash instead of spending or investing, even when interest rates are very low. This usually happens during periods of uncertainty or weak economic confidence, making central bank measures like rate cuts less effective.

Key factors that contribute to a liquidity trap include:

- Deflation: When prices are expected to fall further, people delay purchases because they believe money will be worth more later. This reduces spending and deepens the liquidity trap.

- Balance Sheet Recession: After a recession, households and businesses focus on reducing debt and rebuilding finances rather than spending, which slows economic recovery.

- Low Investor Demand: Companies hesitate to raise funds through stocks or bonds when investment sentiment is weak. At the same time, investors delay decisions due to higher perceived risks.

- Reluctance to Lend: Banks often become cautious about lending during periods of slow economic growth. For example, after the 2008 financial crisis, many banks tightened lending due to liquidity pressures and uncertainty.

How to Overcome a Liquidity Trap

Here are some key measures that can help an economy recover from a liquidity trap:

- Expansionary Fiscal Policy: Higher government spending, along with lower taxes, can stimulate economic activity. This encourages production, supports businesses, and helps revive overall growth.

- Increase in Employment Levels: As government spending rises, job creation improves. Higher employment leads to greater household income and stronger consumer confidence.

- Rise in Disposable Income: With more income available, people are more likely to spend rather than save, which boosts consumption across the economy.

- Growth in Aggregate Demand and Investment: Increased consumer spending encourages businesses to invest and expand, creating a positive cycle of economic activity.

Real-Life Examples of a Liquidity Trap

A liquidity trap typically occurs when very low interest rates coincide with deflation and weak economic confidence, often after major crises such as the Great Depression, Japan’s asset bubble collapse, or the COVID-19 pandemic. In such periods, lower borrowing costs fail to encourage spending or investment.

1. The Great Depression

During the Great Depression, strong deflationary pressures led to a sharp decline in economic activity. Despite lower interest rates, both businesses and consumers held back from borrowing and spending, which deepened the economic slowdown.

2. Japan’s Lost Decade

Japan experienced a prolonged liquidity trap during the 1990s and early 2000s after the collapse of its real estate and stock market bubble. Interest rates fell to extremely low levels, even turning slightly negative around 2002, but investment remained weak, and deflation persisted.

This situation was reflected in the performance of the Nikkei 225, Japan’s key stock index. After reaching nearly 38,000 in December 1989, it remained below that peak for decades.

How Liquidity Traps Influence Market Behaviour

Understanding key economic concepts like a liquidity trap can be very helpful if you plan to invest in the Indian stock market. It helps explain why markets may behave unusually or why the RBI’s policy actions sometimes fail to produce the expected results. With this insight, investors can adjust their strategies and make more informed decisions, especially during periods of economic uncertainty.

FAQs

A liquidity trap occurs when interest rates fall to zero, but people still refuse to spend or invest, preferring to hold cash. Monetary policy becomes ineffective at stimulating economic growth.

In normal recessions, cutting interest rates encourages borrowing and spending. In liquidity traps, rate cuts fail to work because rates already sit at zero, and fear dominates economic behaviour.

India’s growth dynamics, inflation history, and interest rate levels make liquidity traps unlikely. The economy typically responds to rate changes, and positive inflation expectations persist across business cycles.

Fear of deflation, job losses, or economic collapse drives cash hoarding. When people expect prices to fall further, they delay spending. Uncertainty makes cash feel safer than investments.